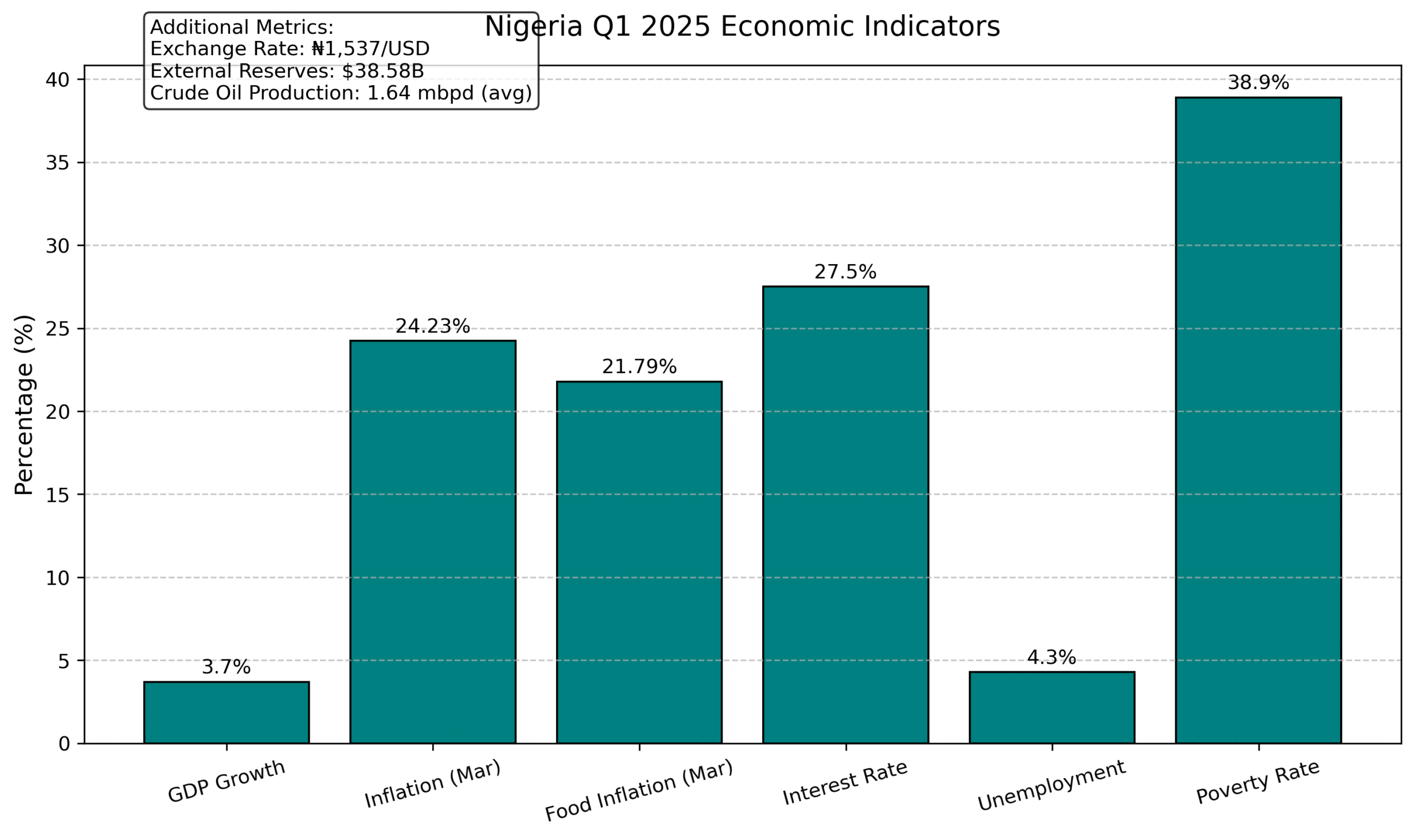

Nigeria’s economy presented a mixed picture in Q1 2025. Navigating the ongoing impacts of 2023’s fuel subsidy removal and FX unification policies. While concerns persist about household and institutional resilience, key data showed moderate GDP growth (3.7%) alongside persistently high, albeit rebased, inflation (24.23% in March). The exchange rate ended the quarter at ₦1,537/USD amid volatility, and while foreign reserves remained relatively stable ($34.8bn), significant challenges like high poverty (38.9%), concerning unemployment realities despite official figures (4.3%), and oil production shortfalls continue to weigh on the outlook. Monetary policy remains tight (interest rate at 27.50%) to combat inflation. Regional expansion (Access Bank in Kenya) and AfCFTA commitments signal strategic positioning, while global market sentiment, influenced by trade tensions and varied Q1 earnings, provides broader context. Addressing structural issues, boosting non-oil exports, and ensuring inclusive growth remain critical priorities.

Despite these shocks, the 2025 outlook presents a cautiously optimistic picture. There are signs of potentially tapering inflation later in the year, a relatively stable exchange rate compared to previous peaks, and moderate growth.

Monetary authorities, particularly the Central Bank of Nigeria (CBN), are expected to sustain interventions aimed at stabilizing the naira and moderating inflation, although the high interest rate environment presents its own challenges.

A breakdown of key Q1 2025 economic data reveals:

- Crude oil production: Averaging between 1.5 to 1.78 million barrels per day (mbpd)

- GDP growth: 3.7%

- Inflation rate (March): 24.23% (Note: Rebased from Jan 2025)

- Food inflation (March): 21.79%

- Exchange rate (end of Q1): ₦1,537/USD

- Interest rate: 27.50%

- Unemployment rate: 4.3%

- Poverty rate: 38.9% (approx. 87 million Nigerians below the poverty line)

- External reserves: $34.8 billion

Review and Assessment of Nigeria’s Economic Domestic Factors

Proposed Budget Review: This move could be beneficial if it enhances infrastructure and productivity. Structural reforms require fiscal responsiveness, and budget adjustments may support that process, provided funds are allocated effectively.

Unemployment Figures: The official 4.3% unemployment rate requires careful interpretation, as it doesn’t fully capture the extent of underemployment or the prevalence of low-paying informal work, which affects a large portion of the workforce. A sustainable job creation strategy must address these underlying realities beyond headline statistics.

Poverty Rate: The fact that nearly 4 in 10 Nigerians live in poverty (38.9%) is deeply concerning. Although GDP growth of 3.7% appears positive, it highlights a lack of inclusiveness, leaving many sectors and demographics behind. Addressing inequality and improving access to education, healthcare, and food security remain urgent priorities.

Inflation Levels: The significant reduction in the headline rate from 34.8% (Dec 2024) to 24.48% (Jan 2025) was primarily due to a statistical rebasing exercise. While necessary for accurate comparison, the subsequent month-on-month increase in March (headline rising to 24.23% from Feb’s 23.18% under the new base) underscores persistent inflationary pressures. Core inflation also rose in March. For improved welfare, sustained price stability reaching single digits is needed. The current high interest rate (27.50%), intended to combat inflation, simultaneously makes borrowing expensive, potentially dampening investment.

Exchange Rate Movement: Post-subsidy removal market unification continues to influence the exchange rate. While unification was necessary, volatility persists (₦1,537/USD at Q1 end), reflecting systemic issues like inconsistent forex inflows and fragile investor confidence, partly influenced by global trade tensions and domestic security concerns. This instability affects purchasing power and hinders non-oil export competitiveness. Stabilizing the FX environment is crucial.

Foreign Reserves: The reserve level ($34.8 billion) is relatively stable but requires bolstering through diversified foreign exchange sources, particularly non-oil exports and diaspora remittances. Nigeria’s heavy reliance on oil makes the economy vulnerable to price fluctuations and production shortfalls. Increasing FDI and building resilience through economic diversification is essential.

Oil Production Shortfall: Production averaging 1.5-1.78 mbpd, below the budget assumption (potentially 2.06 mbpd mentioned elsewhere, though the 2025 budget assumed $75/barrel price), impacts revenue projections. Issues like pipeline vandalism and regulatory delays hinder output. Improving security, infrastructure, and contract enforcement in the oil sector is critical.

Understanding these domestic factors sets the stage for analyzing the specific inflation dynamics and broader economic activity indicators.

Inflation Outlook and Related Economic Indicators

The headline inflation story remains central, standing at 24.23% in March. Food inflation eased slightly to 21.79% (from 23.51% in Jan), but core inflation (excluding food and energy) rose to 24.43% (from 23.01% in Jan), indicating broad-based price pressures. Worryingly, monthly inflation accelerated significantly to 3.9% in March from 2.04% in February.

Fitch forecasts Nigeria’s inflation to average 22% in 2025 and 20% in 2026. Despite central bank hopes for a decline, reaching the single-digit target seems unlikely in the near term. Key drivers include insecurity affecting food supply, the pass-through effects of exchange rate devaluation and fuel subsidy removal, and monetary policies potentially increasing liquidity without commensurate real sector growth.

While many analysts anticipate a gradual decline in inflation in H2 2025, risks remain. Low oil production poses a significant risk; if oil prices fall below budget benchmarks (e.g., $65 mentioned vs. $75 budget assumption), pressure on foreign reserves and the naira could intensify. The next CBN monetary policy meeting (scheduled for May 19th) will be closely watched, with April’s inflation data heavily influencing decisions.

Despite these inflationary pressures, economic activity shows signs of expansion. The overall Purchasing Managers’ Index (PMI) for March was 52.3, marking the third consecutive month of growth, driven by demand and business activity. Stanbic IBTC’s PMI registered 54.3, its highest since early 2024, supported by new orders and employment growth. Beyond domestic indicators, Nigeria is also pursuing regional integration and expansion strategies.

Regional Expansion and Trade Integration

Access Bank, Nigeria’s largest by assets, finalized its acquisition of the National Bank of Kenya from KCB Group, enhancing its footprint in East Africa following approval from Kenya’s Central Bank.

Furthermore, Nigeria submitted its ECOWAS tariff offer under the African Continental Free Trade Area (AfCFTA), committing to eliminating duties on 90% of intra-African trade goods over time. This marks a strategic step toward deeper regional economic integration. These domestic and regional developments occur within a complex global economic environment.

Broader Market Sentiment and Strategic Implications

Global market sentiment in Q1 was mixed, influenced by Q1 earnings reports, ongoing (though slightly easing) trade tensions, and varied inflation data across major economies.

- Economic Sentiment: Germany’s ZEW economic sentiment index saw a historic drop, indicating pessimism, while Canada and the UK saw inflation moderate (2.3% and 2.6% respectively), potentially signaling stable monetary policy ahead. The UK labor market showed resilience.

- Industry Support & Challenges: South Korea announced significant support ($23.2bn) for its semiconductor sector amid global uncertainties. Conversely, Nvidia faced a $5.5bn charge due to export restrictions, impacting its stock. Boeing faced order suspensions from China due to US tariffs, benefiting Airbus.

- Central Bank Stance: South Africa’s central bank noted reduced scope for monetary easing due to global uncertainties, despite projecting lower domestic inflation.

This global backdrop, particularly concerning trade, commodity prices (oil), and investor risk appetite, directly and indirectly impacts Nigeria’s economy through investment flows, export demand, and imported inflation channels.

African Development Bank Group – Nigeria Economic OutlookNBS – Q1 2024 GDPIMF – Nigeria and the IMFNBS – Inflation RatesEconomy of NigeriaFocusEconomics – Nigeria Economic DataAfrican Business – Nigeria’s revamp of economic indicators sparks debateWorld Bank – Nigeria Poverty RateProshare – Nigeria’s External Reserves

Read More: Diaspora Lens